www.aljazeerah.info

Opinion Editorials, September 2012

Archives

Mission & Name

Conflict Terminology

Editorials

Gaza Holocaust

Gulf War

Isdood

Islam

News

News Photos

Opinion Editorials

US Foreign Policy (Dr. El-Najjar's Articles)

www.aljazeerah.info

Why QE3 Won't Jumpstart the Economy and What Would

By Ellen Brown

Al-Jazeerah, CCUN, September 24, 2012

The economy could use a good dose of “aggregate demand”—new spending money

in the pockets of consumers—but QE3 won’t do it.

Neither will it trigger the dreaded hyperinflation.

In fact, it won’t do much at all.

There are better alternatives.

The Fed’s announcement on September 13, 2012, that it was embarking on a

third round of quantitative easing has brought the “sound money” crew out

in force, pumping out articles with frighting titles such as

“QE3

Will Unleash' Economic Horror' On The Human Race.”

The Fed calls QE an asset swap, swapping Fed-created dollars for other

assets on the banks’ balance sheets.

But critics call it “reckless money printing” and say it will

inevitably produce hyperinflation.

Too much money will be chasing too few goods, forcing prices up and

the value of the dollar down.

All this

hyperventilating could have been avoided by taking a closer look at how QE

works. The money created by

the Fed will go straight into bank reserve accounts, and

banks can’t lend their reserves.

The money just sits there, drawing a bit of interest.

The Fed’s plan is to buy mortgage-backed securities (MBS) from the

banks, but according to the Washington Post, this is

not expected to be of much help to homeowners either.

Why QE3 Won’t Expand the Circulating

Money Supply

In its third round of QE,

the Fed says it will buy

$40 billion in

MBS every month for an indefinite period.

To do this, it will essentially create money

from nothing, paying for its purchases by crediting the reserve accounts

of the banks from which it buys them.

The banks will get the dollars and the Fed

will get the MBS.

But the banks’ balance sheets will remain

the same, and the circulating money supply will remain the same.

When the Fed engages

in QE, it takes away something on the asset side of the bank’s balance

sheet (government securities or mortgage-backed securities) and replaces

it with electronically-generated dollars.

These dollars are held in the banks’ reserve

accounts at the Fed.

They are “excess reserves,” which cannot be

spent or lent into the economy by the banks.

They can only be lent to other banks that

need reserves, or used to obtain other assets (new loans, bonds, etc.).

As Australian economist

Steve Keen explains:

[R]eserves are there for settlement of accounts

between banks, and for the government's interface with the private banking

sector, but not for lending from. Banks

themselves may . . . swap those assets for other forms of assets that are

income-yielding, but they are not able to lend from them.

This was also explained by Prof. Scott Fullwiler, when

he argued a year ago for another form of QE—the minting of some trillion

dollar coins by the Treasury (he called it “QE3

Treasury Style”). He

explained why the increase in reserve balances in QE is not inflationary:

Banks can’t “do” anything with all the extra reserve

balances. Loans create

deposits—reserve balances don’t finance lending or add any “fuel” to the

economy. Banks don’t lend reserve balances except in the federal

funds market, and in that case the Fed always provides sufficient

quantities to keep the federal funds rate at its . . . interest rate

target. Widespread belief that reserve balances add “fuel” to bank lending

is flawed, as I explained here over

two years ago.

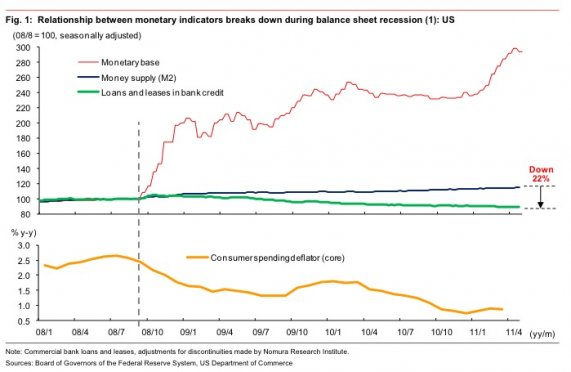

Since November

2008, when QE1 was first implemented, the monetary base (money created by

the Fed and the government) has indeed gone up.

But the circulating money supply,

M2, has not increased any faster than in the previous decade, and

loans have actually gone down.

Quantitative

easing has had beneficial effects on the stock market, but these have been

temporary and are evidently psychological: people THINK the money supply

will inflate, providing more money to invest, inflating stock prices, so

investors jump in and buy.

The psychological effect eventually wears off, requiring a new round of QE

to keep the game going.

That is what

happened with QE1 and QE2.

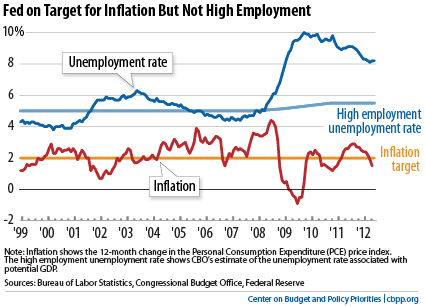

They did not reduce unemployment, the alleged target; but they also did

not drive up the overall price level.

The rate of price inflation has actually been

lower after QE

than before the program began.

Why, Then, Is the Fed

Bothering to Engage in QE3?

If the Fed is doing

no more than swapping bank assets, what is the point of this whole

exercise?

The Fed’s professed justification is that by

buying mortgage-backed securities, it will lower interest rates for

homeowners and other long-term buyers.

As explained in Reuters:

Massive buying of any

asset tends to push up the prices, and because of the way the bond market

works, rising prices force yields [or interest rates] down. Because the

Fed is buying mortgage-backed bonds, the purchases act to directly lower

the cost of borrowing to buy a home. In addition, some investors, put off

by the rising price of the bonds that the Fed is buying, turn to other

assets, like corporate bonds - which, in turn, pushes up corporate bond

prices and lowers those yields, making it cheaper for companies to borrow

- and spend.

Those are the

professed objectives, but politics may also play a role.

QE drives up the stock market in

anticipation of an increase in the amount of money available to invest, a

good political move before an election.

Commodities (oil,

food and precious metals) also go up, since “hot money” floods into them.

Again, this is evidently because investors

EXPECT inflation to drive commodities up, and because lowered interest

rates on other investments prompt investors to look elsewhere.

There is also evidence that commodities are

going up because some major market players are

colluding to manipulate the price,

a criminal enterprise.

The Fed does bear

some responsibility for the rise in commodity prices, since it has created

an expectation of inflation with QE, and it has kept interest rates low.

But the price rise has not been from

flooding the economy with money.

If dollars were flooding economy, housing

and wages (the largest components of the price level) would have shot up

as well.

But they have remained low, and overall

price increases have remained within the Fed’s 2% target range.

(See chart above.)

Some Possibilities That Might

Be More Effective at Stimulating the Economy

An injection of money

into the pockets of consumers would actually be good for the economy, but

QE3 won’t do it.

The Fed could give production and employment

a bigger boost by using its lender-of-last-resort status in more direct

ways than the current version of QE.

It could make the

very-low-interest loans given to banks available to state and municipal

governments, or to students, or to homeowners.

It could rip up the $1.7 trillion in

government securities that it already holds, lowering the national debt by

that amount (as

suggested a year ago by Ron Paul).

Or it could

buy up a trillion dollars’ worth of securitized

student debt and rip those securities

up.

These moves might require some tweaking of the

Federal Reserve Act, but Congress has done it before to serve the banks.

Another possibility

would be the sort of “quantitative easing” first proposed by Ben Bernanke

in 2002, before he was chairman of the Fed—just drop hundred dollar bills

from helicopters.

(This is roughly similar to the Social

Credit solution proposed by C. H. Douglas in the 1920s.)

As

Martin Hutchinson observed

in

Money Morning:

With a U.S. population of 310 million, $31 billion per month, dropped from

helicopters, would have given every American man, woman and child an extra

crisp new $100 bill per month.

Yes, it would produce an extra $31 billion per

month on the nominal Federal budget deficit, but the Fed would have

printed the new bills, so there would have been no additional strain on

the nation's finances.

It would be much better than a new social program,

because there would have been no bureaucracy involved, just bill printing

and helicopter fuel.

The money would nearly all have been spent,

increasing consumption by perhaps $300 billion annually, creating perhaps

3 million jobs, and reducing unemployment by almost 2%.

None of these moves

would drive the economy into hyperinflation.

According to the Fed’s figures, as of July

2010, the money supply was actually

$4 trillion LESS than it was in 2008.

That means that as of that date, $4 trillion

more needed to be pumped into the money supply just to get the economy

back to where it was before the banking crisis hit.

As the psychological

boost from QE3 wears off and the “fiscal cliff” looms, perhaps Congress

and the Fed will consider some of these more direct approaches to

relieving the economy’s intractable doldrums.

_______

Ellen Brown is an attorney and president of the Public

Banking Institute. In Web

of Debt, her latest of eleven books, she shows how a private cartel

has usurped the power to create money from the people themselves, and how

we the people can get it back. Her websites are

http://WebofDebt.com,

http://EllenBrown.com, and

http://PublicBankingInstitute.org.

|

|

|

|

||

|

||||||